Cost Segregation by Property Type:

Which Small Rentals Actually Produce the Biggest Tax Savings?

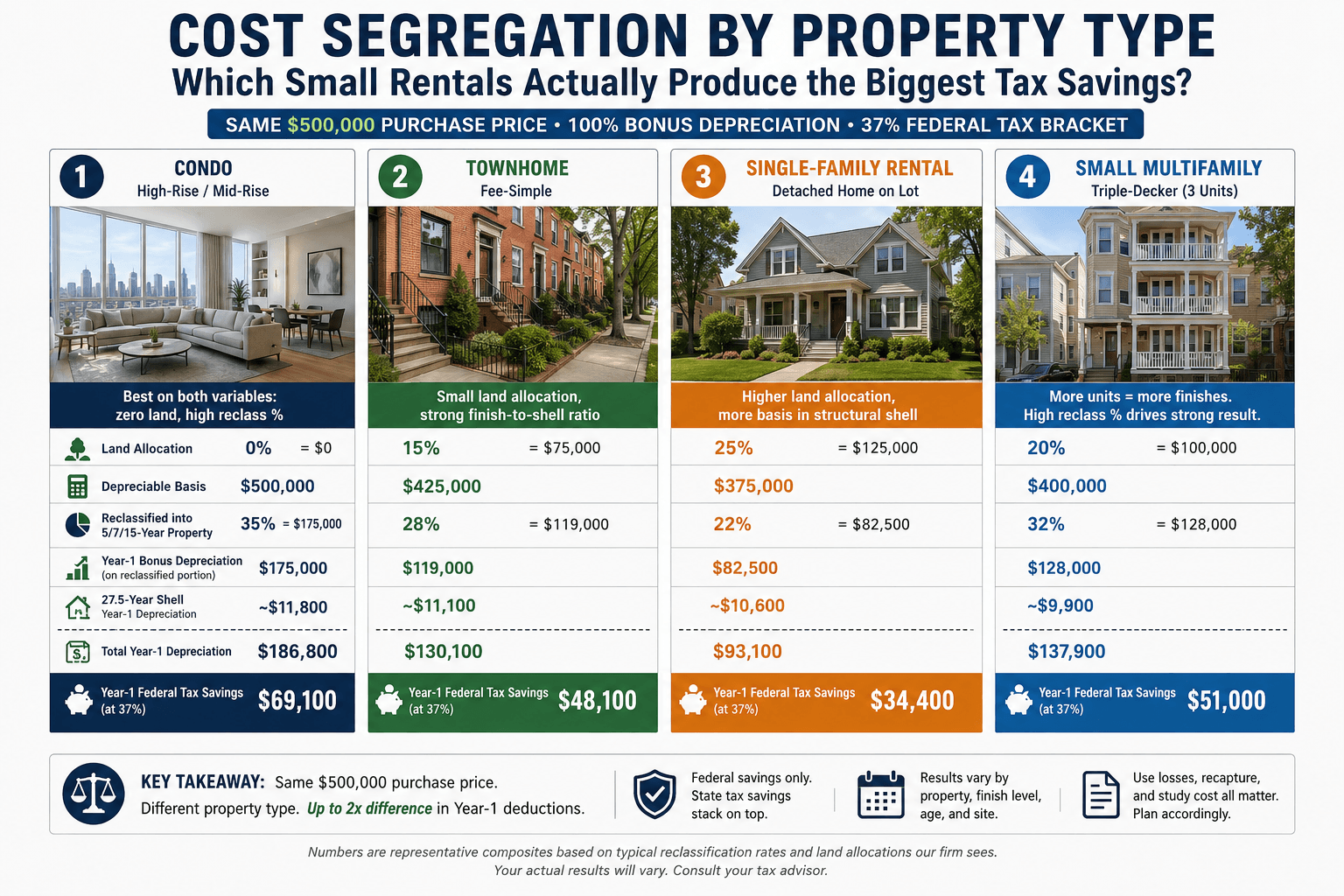

A side-by-side comparison of cost segregation results on a $500,000 condo, townhome, single-family rental, and small multifamily. The differences are larger than most landlords expect.

Cost segregation has become one of the most discussed tax strategies among small landlords in the last few years. BostonApartments.com has covered the basics of accelerating deductions through cost segregation, and the idea is straightforward: instead of depreciating your entire rental over 27.5 years (residential long-term) or 39 years (short-term / lodging classification), an engineering-based study breaks the property into its actual components, reclassifies the short-life pieces (cabinetry, flooring, fixtures, appliances, landscaping, fences, parking) into 5, 7, and 15-year buckets, and lets you deduct most of that in Year 1.

What the introductory coverage rarely shows is the part that actually drives a small landlord's buying decision: how much the result varies by property type. Buying a condo in Back Bay produces a meaningfully different cost segregation outcome than buying a triple-decker in Dorchester or a single-family rental in Brockton. Same purchase price, same study cost, very different first-year deduction. This article walks through that comparison on a $500,000 property across the four property types small Boston-area investors most commonly consider: condo, townhome, single-family rental, and small multifamily.

Quick disclaimer up front: the four scenarios below are representative composites reflecting the typical reclassification rates and land allocations my firm sees on properties of each type. Every property is different, and your study's actual results will vary based on finish level, age, fixtures, land improvements, and the engineer's findings on site. Treat the numbers as a planning framework, not a guarantee.

Why property type matters more than purchase price

Two variables drive a cost segregation result more than anything else: the land allocation (land cannot be depreciated, so it shrinks your depreciable basis) and the reclassification percentage (how much of the depreciable basis the study moves out of the long-recovery shell into 5, 7, and 15-year property). Different property types sit in very different places on both variables.

Land allocation is largely a function of how the property is deeded and where it sits. A high-rise condo deed conveys a unit and a fractional interest in common areas; the land allocation is often functionally zero. A single-family home on a quarter-acre lot in a suburb where land is half the value of the parcel will have a 30%+ land allocation, and that 30% comes straight off your depreciable basis.

Reclassification percentage is largely a function of how much of the building is "finishes" (cabinets, flooring, fixtures, appliances, paint, trim) versus "structural shell" (foundation, framing, roof, exterior walls). A unit that is mostly interior finish with little structural shell on its tax cost basis (a condo) will reclassify higher. A property where a meaningful share of the basis sits in the shell (a single-family home with a large detached garage and a roof you paid for) will reclassify lower.

These two variables compound. The property type with the smallest land allocation and the highest reclass percentage will out-produce the property type at the other end of the spectrum by 2x or more on first-year deductions, even at the same purchase price.

Below: the same $500,000 purchase price, four property types, four very different results. All four assume a long-term residential rental classification (27.5-year shell) and 100% bonus depreciation, which was made permanent by the One Big Beautiful Bill Act in 2025. All assume a 37% federal marginal tax bracket, which is the typical bracket for a high-earning landlord using cost segregation. State tax savings stack on top wherever the household files.

Property Type #1: $500,000 condo

A $500,000 condo in a mid-rise or high-rise building. The deed conveys the unit and a fractional interest in common elements (lobby, elevators, mechanical systems, parking structure) but no deeded land.

- Land allocation: 0% (negligible deeded land)

- Depreciable basis: $500,000

- Reclassified into 5/7/15-year property: ~35% = $175,000

- Year-1 bonus depreciation on reclassified portion: $175,000

- Remaining 27.5-year shell ($325,000): ~$11,800 of Year-1 depreciation

Total Year-1 depreciation: ~$186,800

Federal tax savings at 37%: ~$69,100

The condo wins on both variables. Zero land allocation means the full $500,000 enters the study as depreciable basis. The unit is overwhelmingly finishes (cabinets, flooring, fixtures, appliances), with the structural shell, lobby, and common-area mechanicals carrying very little of the per-unit cost basis. Reclassification rates of 30-40% are normal on condos in well-built buildings.

Property Type #2: $500,000 townhome

A $500,000 townhome, fee-simple (the owner holds title to the unit and the small lot beneath it).

- Land allocation: 15% = $75,000

- Depreciable basis: $425,000

- Reclassified into 5/7/15-year property: ~28% = $119,000

- Year-1 bonus depreciation on reclassified portion: $119,000

- Remaining 27.5-year shell ($306,000): ~$11,100 of Year-1 depreciation

Total Year-1 depreciation: ~$130,100

Federal tax savings at 37%: ~$48,100

Townhomes sit in the middle. The small deeded land share trims the basis modestly. The unit itself still has a healthy finish-to-shell ratio (kitchen, bathrooms, flooring, fixtures), but the shared exterior walls reduce the structural component a unit owner "owns" on paper, so reclass percentages tend to come in slightly below condos. The combination produces a strong but second-place result.

Property Type #3: $500,000 single-family rental

A $500,000 single-family rental on a typical residential lot.

- Land allocation: 25% = $125,000

- Depreciable basis: $375,000

- Reclassified into 5/7/15-year property: ~22% = $82,500

- Year-1 bonus depreciation on reclassified portion: $82,500

- Remaining 27.5-year shell ($292,500): ~$10,600 of Year-1 depreciation

Total Year-1 depreciation: ~$93,100

Federal tax savings at 37%: ~$34,400

The single-family rental gets hit on both variables. Land allocation runs higher (20-30% is typical, sometimes higher in higher-cost-of-land markets) because the owner holds the full lot. The depreciable basis sits more heavily in the shell (full exterior walls, full roof, full foundation, often a detached garage), so reclassification percentages run lower. Single-family rentals still produce real Year-1 deductions, just not at the same magnitude as the property types above.

There is a small offset worth noting: single-family rentals tend to have more land improvements (driveways, fencing, landscaping, exterior lighting, sometimes a pool or deck) than condos or townhomes. Land improvements are 15-year property and bonus-eligible. A property with a paved driveway, mature landscaping, and a fence can pick up an extra 3-5 percentage points of reclass that pushes the result closer to the townhome scenario above.

Property Type #4: $500,000 small multifamily (Boston triple-decker)

A $500,000 small multifamily building, the classic Boston-area triple-decker, a stacked duplex, or a small 2-4 unit building.

- Land allocation: 20% = $100,000

- Depreciable basis: $400,000

- Reclassified into 5/7/15-year property: ~32% = $128,000

- Year-1 bonus depreciation on reclassified portion: $128,000

- Remaining 27.5-year shell ($272,000): ~$9,900 of Year-1 depreciation

Total Year-1 depreciation: ~$137,900

Federal tax savings at 37%: ~$51,000

Small multifamily produces a strong result for a reason that is easy to overlook: more units means more kitchens, more bathrooms, more flooring, more fixtures, more cabinetry, more appliances per dollar of purchase price. A triple-decker at $500,000 has three full kitchens and three sets of bathrooms inside the same shell that a single-family at the same price has one of. That density of short-life components is exactly what cost segregation rewards.

Land allocation is modest because the building footprint covers most of the typical urban lot. The shell takes up roughly the same square footage as it would for a similarly priced single-family, but the interior finish volume per dollar is much higher. The combination of moderate land allocation and high reclass percentage puts small multifamily comfortably ahead of single-family rentals and within striking distance of townhomes.

The comparison side by side

| Property type | Land allocation | Reclass % | Year-1 depreciation | Year-1 federal savings |

|---|---|---|---|---|

| Condo | 0% | 35% | $186,800 | $69,100 |

| Small multifamily (triple-decker) | 20% | 32% | $137,900 | $51,000 |

| Townhome | 15% | 28% | $130,100 | $48,100 |

| Single-family rental | 25% | 22% | $93,100 | $34,400 |

Same $500,000 purchase price, same 37% federal bracket, same 100% bonus depreciation, and the spread between best and worst is roughly 2x on Year-1 deductions. State tax savings stack on top of all four numbers, which widens the absolute dollar gap further for landlords in higher-tax states.

A few things the table does not capture

The comparison above isolates one variable (property type) and holds everything else constant. Real purchase decisions involve a longer list of factors. Three matter enough that they belong in any landlord's planning conversation.

The losses have to be usable. Cost segregation only produces a cash tax benefit if the household can actually use the loss in the year it is generated. For W-2 high earners, that typically requires either Real Estate Professional Status (REPS) for a spouse, the short-term rental loophole if the property is run as a short-stay rental with material participation, or enough passive income from other rentals to absorb the loss. A long-term rental loss without one of those unlocks gets suspended and rolls forward until passive income arrives or the property is sold. The deduction does not disappear, but the timing of the cash benefit shifts. This is covered in detail in the IRS passive activity loss rules.

Recapture matters at sale. When the property is eventually sold, the reclassified personal property gets recaptured at ordinary income rates and the building components are subject to a capped recapture rate. For short holding periods (under 5 years), depreciation recapture can erode a meaningful portion of the original benefit. For long holding periods, the time value of the early deduction overwhelms the recapture; for indefinite holding periods or 1031 exchanges, recapture defers further or never gets paid. Cost segregation works best for landlords who plan to hold for 7+ years or exchange rather than sell.

Study cost and ROI. Engineering-based studies for properties in the $300,000 to $750,000 range typically run $2,000 to $5,000 industry-wide. Against Year-1 federal savings of $34,400 to $69,100 in the examples above, the study cost pays for itself many times over in the first year, before considering state savings. The economics get questionable only on properties under ~$200,000 of depreciable basis, where the absolute deduction is small enough that the study fee eats too much of the benefit.

What this means for a small Boston-area landlord

A few practical takeaways:

If you are comparing acquisition targets across property types and your time horizon is long-term hold, condos and small multifamily produce the best cost segregation economics at the same purchase price. Townhomes are a strong middle option. Single-family rentals are the weakest cost-seg candidates of the four, though far from disqualifying, a $34,000 federal Year-1 deduction is still meaningful, especially when paired with state savings and a long hold.

If you already own properties without cost segregation studies, you can still file a lookback study in any future tax year. The owner files Form 3115 (an automatic accounting method change) and pulls all the missed prior-year depreciation into a single Section 481(a) catch-up deduction in the year of change. No amended returns required. Triple-deckers and multi-unit buildings bought before 2020 are particularly good lookback candidates because the missed depreciation has compounded over multiple years.

If you are considering a renovation, the renovation spend gets classified separately from the original purchase and almost always reclassifies at much higher percentages than the underlying property (renovation dollars rarely go into structural shell). A bathroom remodel can land 60-70% in 5-year property. Planning the study to include the renovation can meaningfully boost the result.

Cost segregation is not a fit for every property or every landlord. But for the right combination of property type, ownership profile, and holding horizon, it remains one of the few legal levers available to small landlords that can deliver five-figure federal tax savings in a single year. The variation by property type is real, and worth modeling before you commit to a purchase.